Our specialty sees contraception as a basic element of women’s preventive care. It helps women determine and space their pregnancies; helps ensure healthier pregnancies; and helps many women with health-care concerns not related to pregnancy to better manage their symptoms and stay healthy.

The drafters of the Affordable Care Act (ACA) recognized the importance of contraception to women’s health when they guaranteed coverage of prescription contraceptives and services, including all methods approved by the US Food and Drug Administration, without deductibles or copays, to millions of women through their private health insurance. This policy was vetted and approved by the Institute of Medicine (IOM) and US Department of Health and Human Services (HHS).

The American Congress of Obstetricians and Gynecologists (ACOG) was central to these discussions. ACOG Executive Vice President and CEO Hal C. Lawrence III, MD, offered our women’s health guidelines and guidance to the IOM, the entity designated by the Secretary of HHS to recommend exactly what coverage and services should fall within the category of women’s preventive care. ACOG’s recommendations were broadly accepted by IOM and HHS and are now required coverage for women across the nation.

Related Article: ACOG to legislators: Partnership, not interference Lucia DiVenere, MA (April 2013)

So, why the confusion and controversy?

Let’s clear up the confusion first.

We’ve heard that private health plans now are required to cover contraceptives without cost sharing. But it’s a little more complicated than that.

It’s true that the ACA requires new private plans to cover a broad range of preventive services:

- evidence-based screenings and counseling

- routine immunizations

- childhood preventive services

- preventive services for women.

Did you catch the word “new” in that sentence?

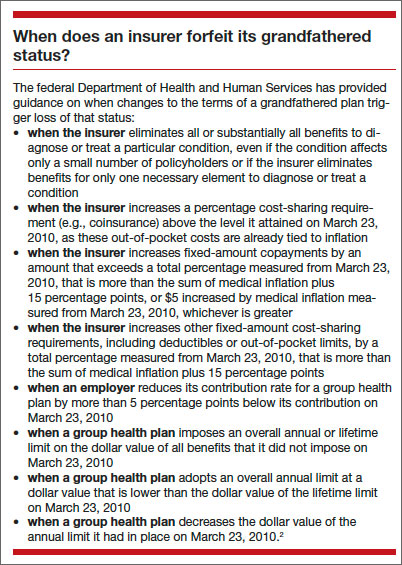

Health plans that existed before March 23, 2010—the date the ACA was signed into law—and that haven’t changed in ways that substantially cut benefits or increase costs for consumers are considered “grandfathered plans” and are not required to abide by these and other requirements in the law.

There are two types of grandfathered plans:

- job-based plans—health insurance plans administered through employers can continue to enroll people as long as no significant changes are made to coverage

- individual plans—a grandfathered plan purchased by an individual cannot expand coverage beyond that individual.

Any insurer can cancel a grandfathered plan as long as it provides 90-day notice to the plan’s enrollees and offers other coverage options. Because grandfathered plans are exempt from a number of ACA benefits and protections, these plans are required to disclose their status to their enrollees.

The number of people enrolled in grandfathered plans is steadily decreasing. In 2013, 36% of people covered through their jobs were enrolled in a grandfathered health plan, down from 48% in 2012 and 56% in 2011, according to the Kaiser Family Foundation.1 Here’s a quick look at the consumer protections that do and do not apply to grandfathered plans.

All health plans must:

- end lifetime limits on coverage

- end arbitrary cancellations of health coverage

- cover adult children up to age 26

- provide a Summary of Benefits and Coverage, a short, easy-to-understand summary of what a plan covers and costs

- spend revenue from premiums on health care, not on administrative costs and bonuses.

Grandfathered plans don’t have to:

- cover preventive care for free, including contraceptives

- guarantee your right to appeal

- protect your choice of doctors and access to emergency care

- be held accountable through Rate Review for excessive premium increases.

Nor do grandfathered individual plans (the kind you buy yourself, not the kind you get from an employer) have to end yearly limits on coverage or cover a preexisting health condition.

Right away, then, we have a situation in which some patients may have 100% coverage for contraceptives while others don’t, especially if their plans were in effect before the ACA became law.

There’s a second segment of your patient population that may not have full contraceptive coverage: those who are covered through employment with a religiously affiliated nonprofit. Initially, in August 2011, only health insurance provided through employment with houses of worship was exempted from the requirement to cover contraceptives. In July 2013, this exemption was expanded to address concerns from other religious affiliates, including universities and hospitals.

This “accommodation,” as it’s known, exempts religiously affiliated nonprofits with religious objections from contracting, arranging, paying for, or referring for contraceptive coverage for their employees. Instead, their insurers are required to provide this coverage free of charge to the employer or employees—an attempt to ensure that all women have the same access to care, regardless of their employment setting. This accommodation is available only to organizations that: