Whether these varying types of state regulation lead to higher or lower premiums is unclear.

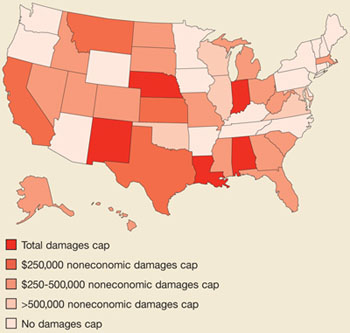

In addition to these strategies, states have also implemented an array of tort reforms in an attempt to address the cost of physician malpractice policies. Caps have been the most popular reform, with 26 states instituting them (FIGURE 2).3

FIGURE 2

Caps on damages by state

Recent events influencing premiums

A number of changes in the past few years have occurred in the malpractice arena

- Increased numbers of physician-owned companies and fewer commercial carriers since the malpractice crisis of the 1970s. These companies often give physicians better rates and more control, but some have been undercapitalized and not survived.

- A rise in the cost of reinsurance since September 11. Reinsurance covers costs above a certain level and limits companies’ losses in a given year. Reinsurers suffered large losses from the terrorist attacks of September 11, 2001 and, subsequently, raised their prices significantly to all liability companies.

- More hospitals self-insuring to better control rates and their risk pool leading increasing numbers of physicians to obtain their malpractice coverage through hospitals. This lowers their costs in comparison to those who practice in small groups or solo settings.

- A shift in the type of insurance from occurrence (all incidents in the policy year are covered regardless of when the claim is filed) to claims-made policies (coverage is for claims filed in the policy year regardless of when the event occurred). With claims-made insurance, physicians have to purchase costly “tail” policies to cover the possibility of incidents during the years of coverage becoming future claims.

- The growth of state-mandated funds as insurers of last resort for physicians who cannot find any coverage. These funds are financed by surcharges on hospital and physician malpractice policies, which in turn increases those costs.

- A decrease in companies’ investment yields since 2000 (from 5.2% in 2000 to4.3% in 2002), in spite of the fact that insurers’ portfolios are quite conservative as required by state law. While some companies saw their investment income drop by 50% in these years, this amount is still only a small part of insurers’ total income.

Options to explore

- Check with your state’s division of insurance website to see if there is a list of carriers, and information about their experience.

- Rather than a claims-made policy, consider getting an occurrence policy that will eliminate the worry and cost of purchasing “tail” insurance. If you work for a group practice, inquire about whether occurrence insurance is an option. If occurrence insurance is not available or seems too costly, ask your agent about what a typical tail policy would cost.

- You may want to inquire about purchasing insurance through a local hospital, which could yield cost savings.

- Don’t skimp on coverage amounts. Consider getting risk-management training to learn what you can do to minimize the risk of being sued.

The current malpractice crisis

Insurance becomes less available when carriers exit the market because of decreased profitability, as happened in the first malpractice crisis (1974–76) and in the current crisis in which St. Paul, the largest national malpractice insurer, left the market.

Insurance becomes less available when carriers exit the market because of decreased profitability, as happened in the first malpractice crisis (1974–76) and in the current crisis in which St. Paul, the largest national malpractice insurer, left the market.

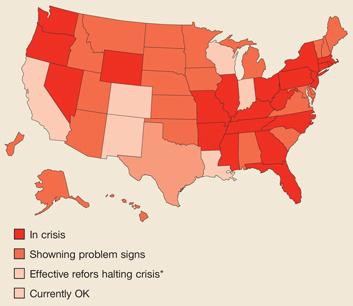

A malpractice crisis, according to the AMA, occurs when “patients lose access to care as a result of a broken medical liability system… that causes physicians’ insurance premiums to skyrocket forcing them to restrict their practice.” An alternate description would be when insurers’ financial situation deteriorates resulting in higher than average increases in premiums or decrease in the supply of insurance. The existence and severity of a crisis varies from state to state (see map at right).4

Insurance becomes relatively unaffordable when premiums increase rapidly, as occurred in the second malpractice crisis in the mid-1980s and also in the current crisis, which has seen increasing premiums since 1999 and some moderation since 2004. Increases in premiums may differ across states, within states, and among specialties.

How providers feel about premium increases depends on both the size and rapidity of the increases and by their ability to collect more for their services to pay for increases. In the current crisis, providers have had more difficulty maintaining a balance between cost increases and income as discounted fee contracts and lack of growth in Medicare and Medicaid payments have constrained growth in practice revenue.

CORRESPONDENCE

Eric A. Henley, MD, MPH, Department of Family and Community Medicine, University of Illinois College of Medicine at Rockford, 1601 Parkview Avenue, Rockford, IL 61107-1897. E-mail: ehenley@uic.edu